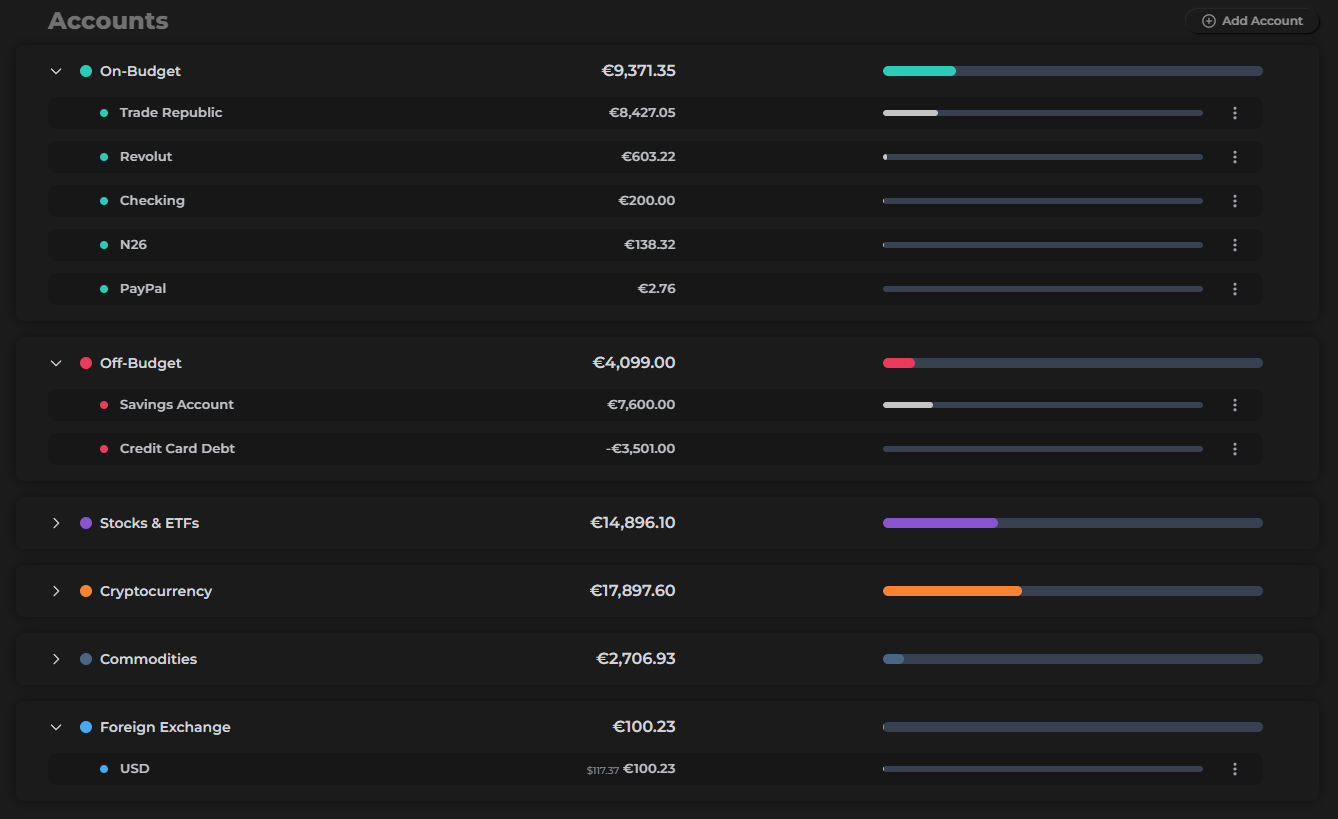

Account Types

Finzen has three account types — each plays a distinct role in how your financial data is organized and which parts of the app it powers.

At a glance

| Account Type | Best for | Affects budget? | Affects net worth? | Affects portfolio? |

|---|---|---|---|---|

| On-Budget | Checking, cash, PayPal | ✓ | ✓ | — |

| Off-Budget | Savings, loans, debt | — | ✓ | — |

| Investment | Stocks, crypto, commodities, forex | — | ✓ | ✓ |

On-Budget accounts

On-Budget accounts are your everyday financial accounts — checking, cash, digital wallets, neobanks. These are the accounts your money flows through on a daily basis.

Every transaction logged to an on-budget account feeds directly into your envelope budget. When you buy groceries and log it against your checking account, the Groceries envelope goes down. This is the core loop that makes budgeting work.

On-budget accounts are also the source for spending reports — daily totals, spending by category, cash flow in and out.

If you regularly spend from it, it should be on-budget. When in doubt, on-budget is the right default for a new account.

Off-Budget accounts

Off-Budget accounts are tracked for your net worth but kept separate from the envelope budget. Think savings pots, emergency funds, loans, or lines of credit you want to monitor without mixing into your daily spending picture.

They're still denominated in your primary currency, and their balances factor into your total assets and liabilities — but no transactions you log here will affect your budget envelopes.

Transfers between on-budget and off-budget accounts are handled intelligently:

- Moving money to an off-budget account with a positive balance → treated as savings

- Moving money to an off-budget account with a negative balance → treated as a debt payment

This means sending money to your savings fund and paying off your credit card are both modeled correctly — without you having to set anything up. They also affect your savings/debts budget subcategories accordingly.

A loan or credit card with a negative balance belongs in Off-Budget, not On-Budget. This keeps your debt payments out of your spending envelopes and lets them show up properly in cash flow.

Investment accounts

Investment accounts live in their own section of Finzen and power the Portfolio report. Unlike the other account types, their value is driven by live market prices — you enter how many units you hold, and Finzen calculates the current value automatically.

Supported asset classes:

- Stocks, ETFs, mutual funds, futures — 15,000+ stocks, 5,000+ ETFs, 10,000+ mutual funds, 2,000+ futures

- Crypto — 10,000+ cryptocurrencies

- Commodities — physical gold, silver, copper, palladium (in grams)

- Forex — 150+ currency pairs

Investment accounts contribute to your net worth at market value, but they're never part of the envelope budget or spending reports. Performance, P&L, allocation, and risk metrics all live in the Portfolio section.

How they work together

Every part of the app draws from a specific account type, so the numbers are always meaningful:

- Spending reports → on-budget accounts only

- Portfolio reports → investment accounts only

- Net worth → all three, combined

- Cash Flow / Sankey → separates budget spending, savings transfers, and debt payments into clearly labeled flows

The result is a financial picture where each layer — spending, saving, investing — is always visible, always clean, and never tangled up with the others.

This separation isn't just organizational. It reflects how money actually moves through your life: money you spend, money you save, and money you grow. Finzen keeps these three flows distinct so you always know exactly what's happening.

Where to go next

- Investment Accounts — adding and managing your investment positions in detail

- Managing Your Budget — how on-budget accounts power your envelope budget